‘Our 17 properties will lose £16,000 per year’

Offered no respite in the Budget, landlords are facing a bleak future and a conundrum over how to manage their properties. Existing landlords are caught between an income tax bill which is set to begin rising next year, or the stamp duty hit involved in incorporating their properties now.

Shirleyann Haig, who owns 17 properties in Liverpool, is in this situation. She and her husband Matt are facing long-term financial ruin if they don’t incorporate – or a big tax hit now if they do.

There are three main tax policies that are likely to affect landlords’ profitability – all of which are making the future look bleak for the Haigs.

First, in an unexpected move, the Chancellor, George Osborne, excluded them from a drop in capital gains tax for both higher and basic-rate taxpayers.

He also confirmed that a 3pc surcharge in stamp duty will go ahead from April 1, as planned in consultation, and scrapped a planned stamp duty exemption for larger landlords, meaning those with more than 15 properties already will also have to pay the extra tax.

And from April next year landlords will not be able to deduct their mortgage interest payments from their rental income before calculating their tax bill.

They will effectively be paying tax on their turnover, instead of their profit, and as a result many will suffer a plunge in profit or fall into the red.

Alan Ward, chairman of the Residential Landlords Association, said: “The decision in the Budget to cut capital gains tax for nearly all assets other than residential property, on top of Stamp Duty changes, is a further assault on rented housing in an attempt to wrongly make landlords the fall guys for the housing crisis.

“We need 1 million new homes to rent by 2020 and all the Government’s action will do is to deter investment creating an even worse shortage and so drive up rents.”

- Buy-to-let: How to set up as a company to save tax, and when it’s worth it

- ‘The Government’s buy-to-let tax changes mean I will have to sell – or raise rents’

Would investing in buy-to-let via a company salvage some of your returns?

At the moment, landlords who own their properties through a company – rather than in their own names – are not going to be hit by the change in the treatment of mortgage interest.

But higher mortgage interest rates applying to company borrowers, combined with set-up costs, mean that setting up a special company – “incorporating” – may not help.

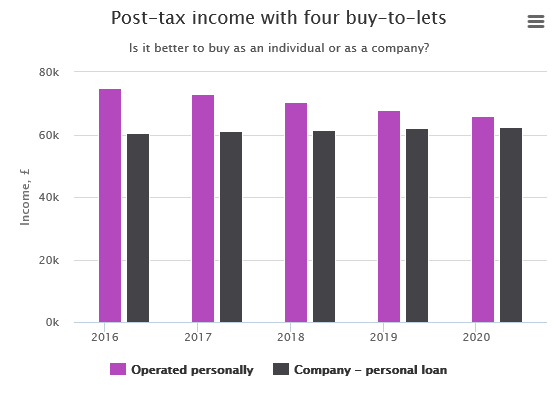

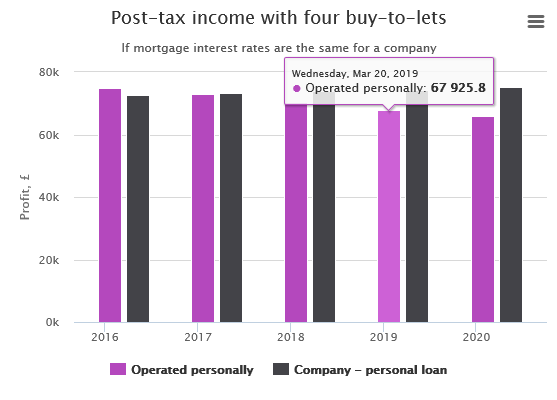

Figures from accountants Smith & Williamson show that a landlord buying four properties in his own name could see his income drop 14pc by 2021 (when the tax change is fully implemented) if he doesn’t incorporate.

If he does incorporate, his profits start at a lower level today and recover slowly toward 2021.

The calculations take a theoretical buy-to-let investor earning £58,000 from his day job. He buys four properties, each costing £380,000 and each being mortgaged at 75pc of their value at a rate of 2.54pc.

He receives £19,200 a year in rental income on each (a yield of just over 5pc).

In year one, after all mortgage costs and taxes are taken into account, his total net income is £74,881.

By 2021, when the ability to deduct mortgage interest relief is fully removed and replaced instead with a 20pc tax credit, his net income will have fallen to £65,790

Now assume the same investor buys via a company. The problem is that the mortgage rates are higher at 4.5pc, so his post-tax income drops immediately to £60,496.

That level of income remains unaffected by the changing tax treatment of mortgage interest. One the face of it, a borrower in these circumstances will be worse off using a company structure.

If average interest rates offered to landlords in corporations come down –a trend that many brokers are predicting – this could be a more viable option. Equally, landlords with smaller borrowings will fare differently.

What about properties you already own?

For landlords who already own multiple properties, the benefits of incorporating – such as they are – are difficult to capture.

That is because capital gains tax may apply when properties are sold by the individual, and stamp duty when they are repurchased by his company.

Jonathan Grant, 36, is facing an increasing tax bill on his four properties in London and Berkshire from next year.

He hopes that political ambition might prompt an about-turn by George Osborne, who will need the votes of “mainly Conservative” landlord investors.

“I think he might change his mind if he wants to be Prime Minister,” said Mr Grant.

“I was very disappointed that there was no reversal on stamp duty. I was looking at buying a block up north somewhere, but I’ll now have to pay the 3pc stamp duty surcharge on that so I probably won’t do it,” he said.

The tax change will mean our 17 properties will lose us £16,000 per year

Shirleyann Haig has a large portfolio of buy-to-let properties which currently break even. After the Government’s changes she will be plunged into losses of around £16,000 per year, she reckons – unless she can sharply increase rents.

At 39 the mother-of-two owns 17 buy-to-let properties on the council estate where she grew up, in Knowsley, Liverpool.

All the properties are mortgaged at around 70pc of their price and they are jointly owned by her and her husband Matt, 37.

The mortgage interest payments come to £80,000 a year and are split between the couple.

The changes will mean that both become higher-rate taxpayers, and their tax bill is set to rocket. But if she wanted to incorporate the business, the bill would be around £100,000 in stamp duty and set-up costs.

The cost of incorporating

Shirleyann Haig’s £95,440 bill

- Mortgage fee £20,800

- Valuation £6,000

- Lender legal £3000

- Broker fee £2000

- Solicitors £22,000

- Stamp duty £41,640

- Plus capital gains tax

Mrs Haig said: “I thought I was helping people with this business, but I’ve ruined my own life by taking a decision which I thought would be good. And then the Government decided landlords were the devil.”

“We used every single penny of our savings, and we don’t make much money from the properties. Last year they broke even on paper.

“It’s very different in the North to how it is in the South East: we can’t rely on the capital growth.”

The Haigs have worked out that if they don’t incorporate, their extra tax liability would leave them a staggering £16,000 a year out of pocket by the time it has been fully implemented.

Mrs Haig said: “We take on vulnerable, high risk, homeless, people who can’t get into social housing. We do not exceed the housing benefit allowance. If people’s circumstances change, we drop the rent.”

To make matters worse, the family are immediately going to be hit by the stamp duty tax hike when it comes in at the start of April, as they are currently renting their own home – and are wanting to buy.

Because they already own property, they will have to pay the 3pc stamp duty surcharge.

Mrs Haig said: “I’ve changed jobs so it’s been hard to get a mortgage. I’ve got the kids in school and I’m ready to buy now – but it’s going to be a struggle to get it through before April 1.

“One day late and I’ll have a tax bill of £11,000. We can’t afford that so we’d have to pull out. We could be left homeless if someone else wants to buy it.”

If you have any comments, please email the author of this article and click on the link above